If you're starting out, Dubai Real Estate Investing for Beginners can feel overwhelming: dozens of neighborhoods, countless developers, and a flood of online promises. This guide answers the 26 most practical questions every new investor asks — from whether now is a good time to buy, to how to pick the right unit, how payments and ownership work, and how to actually make money from your property.

Part 1 — Should you invest now?

Short answer: yes. Prices in Dubai have recovered strongly, yet average per‑square‑foot values are still near levels seen a decade ago. That gap hides a major change: Dubai today is more livable, better regulated, and far more attractive to global buyers.

Three practical reasons to consider investing now:

- Relative affordability: payback from rental income is typically faster than many global cities (roughly 15 years vs 20–40+ elsewhere).

- Strong demand: tourists and high‑net‑worth buyers view Dubai as a top destination — tourism numbers are at record highs and high‑net‑worth interest is substantial.

- Investor benefits: property ownership can unlock residency and golden visa options (details below).

Residency and golden visas

Two common routes:

- Investor visa: buy property worth at least AED 750,000 (about $200,000) for a 2‑year renewable residency. You must visit the UAE at least every six months to maintain the visa.

- Golden visa: requires property worth AED 2,000,000 (around $546,000). Recent changes allow qualifying with a 20% down payment plus the 4% DLD fee, so you may secure long‑term residency before completion. Golden visa holders can include parents and have fewer age limits for children.

How much money do you need?

Dubai's market covers wide budgets. Typical entry points:

- Affordable tier (areas like JVC, Arjan, Sports City): studios $150k–$220k; one‑beds $200k–$340k.

- High end (Downtown, Creek Harbour, Dubai Hills): one‑beds $400k–$800k; two‑beds $620k–$2M.

- Luxury (Palm, Emirates Hills, Bluewaters): starting roughly $1M and up — villas can reach $50–60M.

Acquisition and recurring costs

Expect additional fees beyond purchase price:

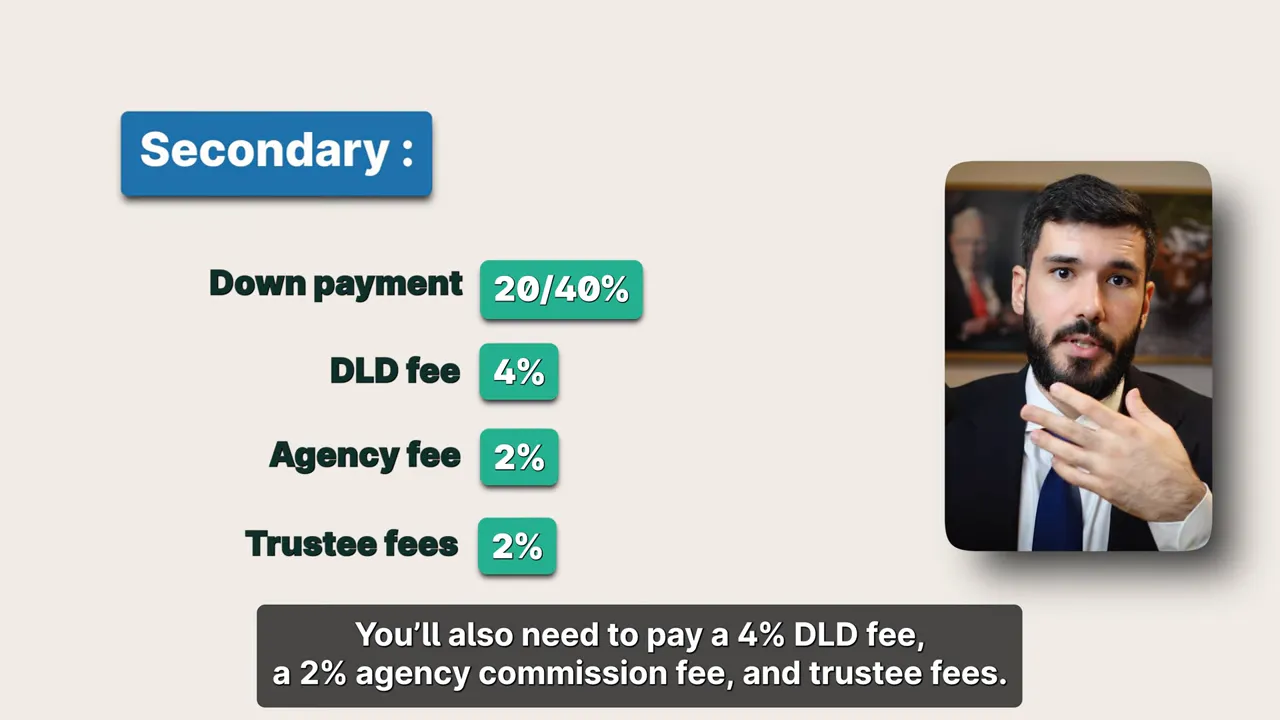

- Acquisition: Dubai Land Department (DLD) transfer fee is 4%. Off‑plan purchases also include developer admin fees (example: ~$15,000). Secondary market adds ~2% agency commission plus trustee and legal fees (~$5,000 combined).

- Running costs: service charges typically $3–$6 per sq ft per year (one‑beds ~$2.5k–$4k annually); housing fee is 5% of assessed annual rent if not rented; utilities if occupied privately.

Can the property be taken from you?

Ownership types matter. Freehold ownership means you fully own the property and can pass it on. Leasehold is effectively a long lease (commonly 99 years) and is less common for new projects. Freehold dominates the current market, so risk of losing title is low when you follow standard procedures.

Part 2 — Picking the right property

Evaluate properties by aligning them with your investment goal, not by price alone.

- Define your goal: capital appreciation, rental income, residency, or a mix.

- Check comparables: for ready units, look at actual transaction prices in the building; for off‑plan, benchmark similar projects in the area.

- Estimate income: research current rents for comparable units and factor service charges.

- Calculate metrics: ROI and cash‑on‑cash return, then compare options.

Best areas (general guidance)

- For rental yield: JVC and Arjan often deliver strong rent‑to‑price ratios (7% average; up to 9–10% in top projects).

- Growth potential: Creek Harbour and Dubai Hills — large projects and new infrastructure still to be delivered.

- High‑end future plays: Oasis, Bamar, and Dubai Islands — these are early stage and target premium buyers.

Top developers to watch

Reputation and masterplan control matter. Notable developers include:

- Emaar — large master communities, sustained demand.

- Nakheel — created some of the most lucrative beachfront assets historically.

- Meraas — premium lifestyle developments and differentiated projects.

Should you buy off‑plan or secondary?

Both can work. Choose based on these rules of thumb:

- Off‑plan is best if you need flexible, interest‑free payment plans, want earlier stage entry, or cannot secure a mortgage. Off‑plan often appreciates during construction.

- Secondary is best if you need immediate rental income, prefer a ready asset, or can access a mortgage (residents typically get 20% down, non‑residents ~40%).

Part 3 — Paying and closing the deal

Key practical points when closing:

- Negotiation: Ready properties are more negotiable; developers may discount for larger down payments, strict payment plans, or bulk purchases.

- Upfront payments (typical): Off‑plan booking sums from ~$7–10k, 10% on booking, 20% down payment (including booking), plus 4% DLD fee and admin fees. Secondary purchase: down payment depends on mortgage/residency status.

- Payment methods: local payments in developer offices, SWIFT transfers, online card checkout, and some developers accept crypto.

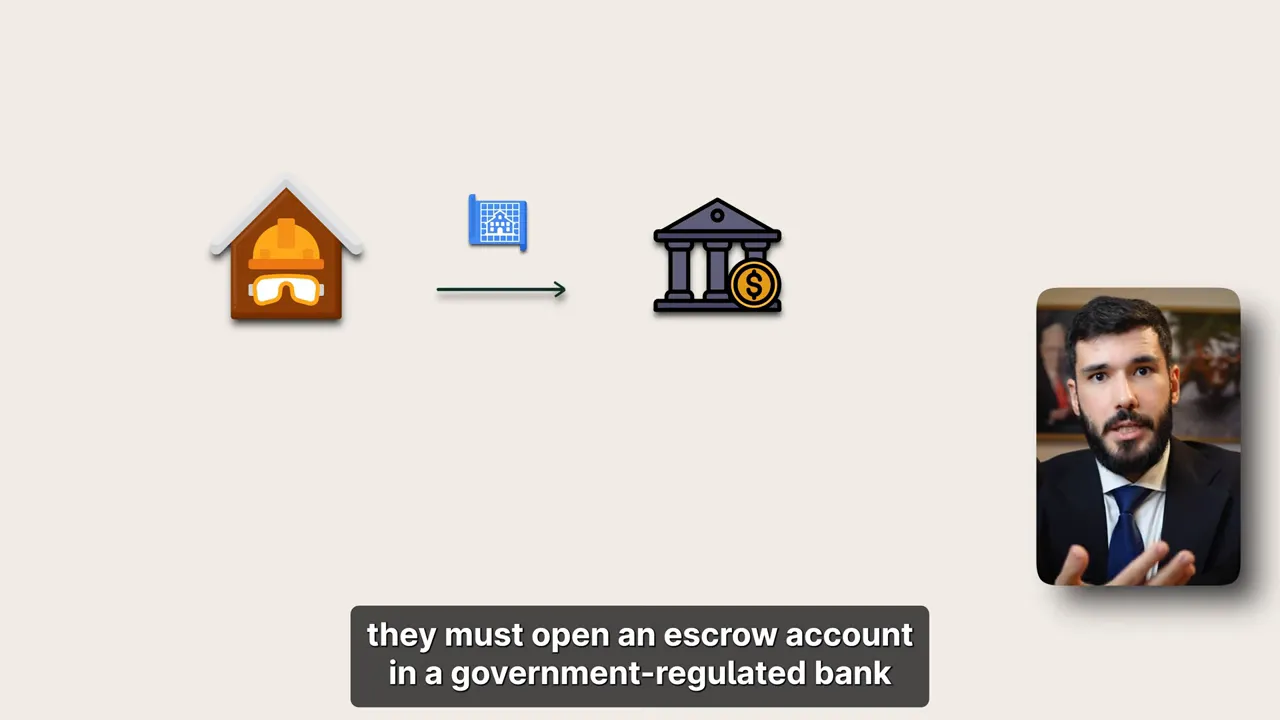

Escrow protection and developer risk

New projects require escrow accounts and bank guarantees. Buyer payments flow into escrow and are released to developers only as construction milestones are met. This is a major protection against developer insolvency.

Part 4 — Making money: renting, reselling, ROI

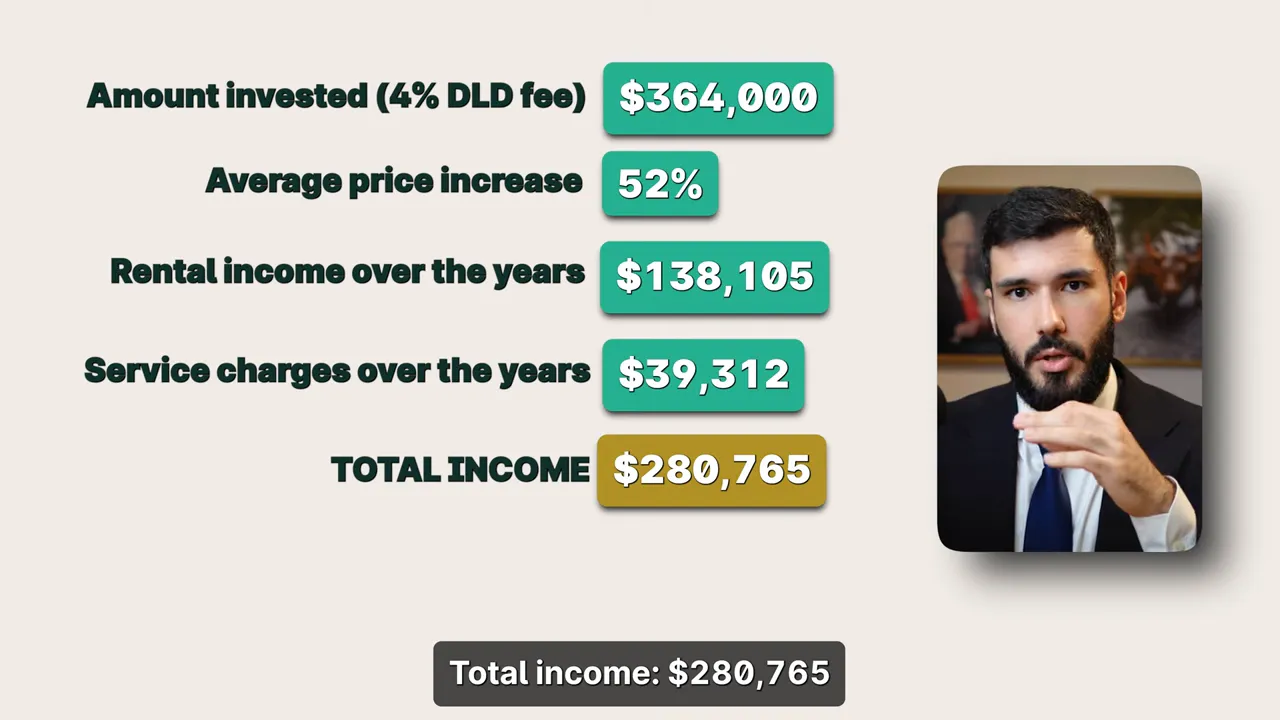

How much can you make? It varies by asset and timing, but historical examples illustrate potential:

- An average apartment bought in 2016 and sold recently could show around 177% total return (including price rise and rental income).

- Villas and prime beachfront assets have shown even higher returns — some Palm Jumeirah villa investments delivered 200%+ ROI over several years.

Resale during construction

You can resell off‑plan units, typically after paying 30–35% of the price. Profit and liquidity depend on demand for that specific asset; unique, highly sought units resell best.

Renting and property management

Long‑term rentals are commonly unfurnished or semi‑furnished; tenants pay utilities and housing fees. Rental payments are typically issued via dated checks. For short‑term rentals, furnish the unit and consider a professional management company — expect management fees around 20% of rental revenue plus utilities and housing fees.

Selling process and costs

- Agree terms with your agent and sign a brokerage agreement.

- Market the property and arrange viewings.

- Sign the memorandum of understanding when a buyer is confirmed; buyer provides at least 10% deposit.

- Obtain a No Objection Certificate from the developer (usually up to $1,000).

- Complete transfer at a trustee office; DLD fees typically paid by buyer. Seller costs are usually agency commission and the NOC fee.

Final checklist for beginners

- Decide your main goal: cash flow, capital growth, residency.

- Research comparables and service charges for any unit you consider.

- Prefer projects with escrow protection and reputable developers.

- Plan financing early: off‑plan payment plans vs secondary mortgages.

- Factor all fees: DLD 4%, agency commission, service charges, NOC cost, and possible trustee/legal fees.

Dubai Real Estate Investing for Beginners doesn't need to be confusing. With clear goals, reliable data, and a checklist, you can make informed decisions and build a property portfolio tailored to your needs.